MTD – THE ESSENTIALS

As you may have seen through the national media “Making Tax Digital”, or MTD as it is commonly known, is almost upon us. MTD represents a major change to the UK tax system.

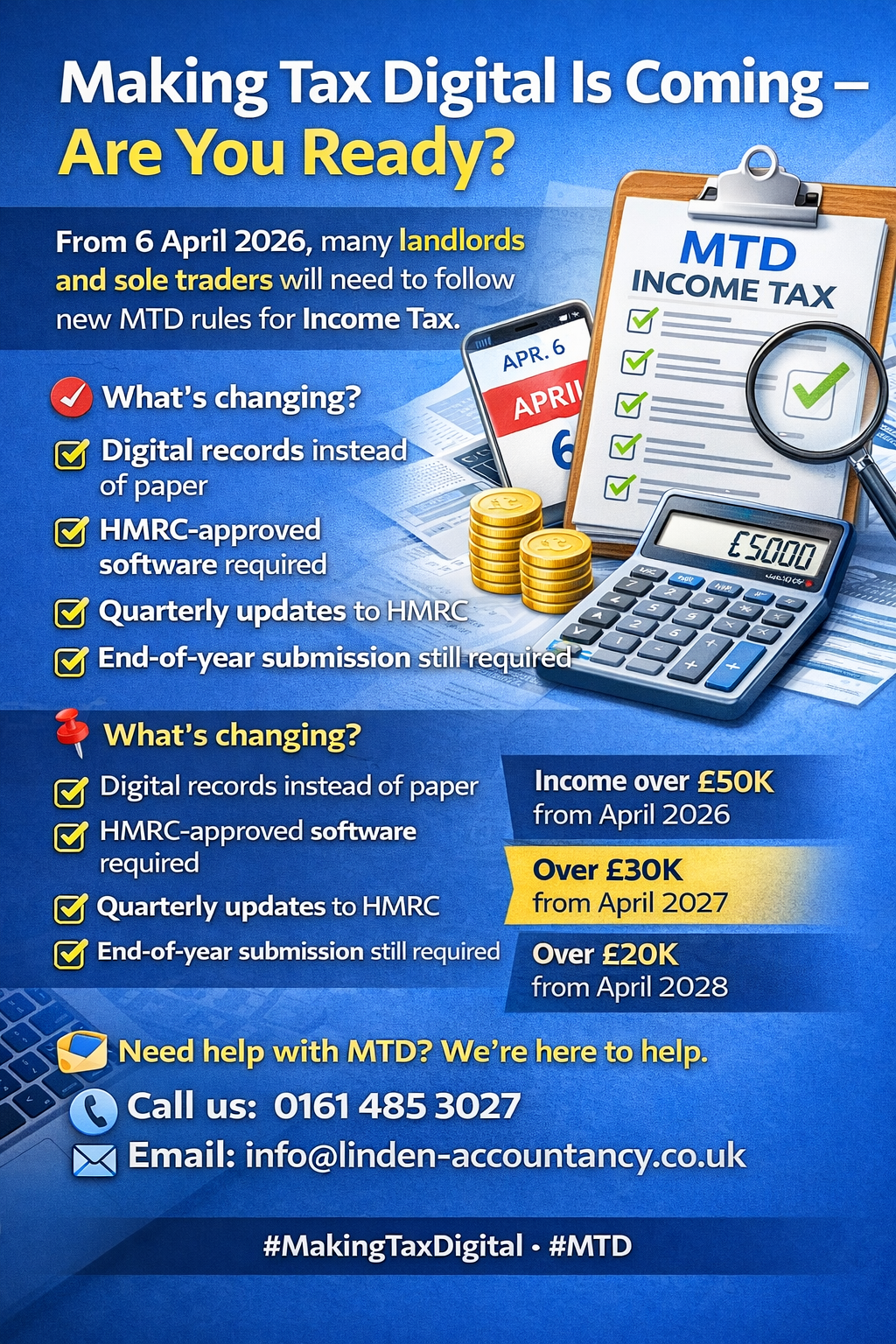

When Is Making Tax Digital Being Introduced?

MTD is being introduced in three stages over the next three years for sole traders and landlords as follows:

Tax year ending — 5 April 2027

Threshold for qualifying income for MTD — £50,00

Qualifying income from tax return for year ending — 5 April 2025

Tax year ending – 5 April 2028

Threshold for qualifying income for MTD — £30,00

Qualifying income from tax return for year ending — 5 April 2026

Tax year ending – 5 April 2029

Threshold for qualifying income for MTD — £20,00

Qualifying income from tax return for year ending — 5 April 2027

Please note that at present the MTD commencement date for partnerships has not been announced. In addition, HMRC have confirmed that MTD will not now apply to limited companies.

As noted above the first group of sole traders and landlords to whom MTD will apply will be those whose gross income (before deduction of expenses) was over £50,000 in the tax year ending 5 April 2025 i.e. for the last tax return submitted.

For individuals who are both sole traders and landlords, gross income is calculated as trading income plus gross rents, all before expenses and deductions.

Therefore, if your gross income as declared in your tax return for the year ended 5 April 2025 was more than £50,000 you will need to register for MTD.

What Does Making Tax Digital Involve?

If your income is above the relevant threshold (see above) you will need to register for Making Tax Digital from 1 April 2026 (if you are a sole trader and your accounting year end is 31 March) or 6 April 2026 (if your accounting year end is 5 April).

We will be arranging this on behalf of our existing clients.

You will also be required to comply with the MTD for Income Tax Self-Assessment regulations and need to:

- Keep digital records of their business income and expenses

- Use compatible software to maintain and process those records

- Submit quarterly returns or “updates” of your income and expenses to HMRC instead of only one annual tax return

- Submit a fifth annual return incorporating income declared from your quarterly returns plus other income sources.

- This means that instead of submitting one tax return for each tax year you will now need to submit 5 tax returns.

This will change how your tax information is recorded and reported and may require setting up suitable accounting software after completing official MTD registration.

When Will Quarterly Returns need to be submitted?

If calendar quarters are used to simplify reporting (which HMRC does allow), you will need to be registered by 1 April 2026 to ensure everything is set up and ready for the first quarterly update.

The applicable quarterly dates and due dates for submission of the quarterly returns are as follows:

Period 1: 1 April — 30 June (submission deadline – 7 August)

Period 2: 1 July — 30 September (submission deadline – 7 November)

Period 3: 1 October — 31 December (submission deadline – 7 February)

Period 4: 1 January — 31 March (submission deadline – 7 May)

For sole traders and landlords using 5 April year ends the quarterly dates are:

Period 1: 6 April — 5 July (submission deadline – 7 August)

Period 2: 6 July — 5 October (submission deadline – 7 November)

Period 3: 6 October — 5 January (submission deadline – 7 February)

Period 4: 6 January — 5 April (submission deadline – 7 May)

The deadline for the submission of the final annual MTD return will remain 31 January immediately following the relevant tax year end. For example, the submission deadline for the return for the year ended 5 April 2027 will be 31 January 2028.

When Will Tax Due Dates Fall?

At the moment payment dates for MTD will be the same as for self-assessment tax returns i.e.

- First payment on account — 31 January during the relevant tax year

- Second payment on account — 31 July following the end of the tax year

- Balancing payment — 31 January following the end of the tax year

For example, the due dates for the tax year ended 5 April 2027 will be:

- First payment on account — 31 January 2027

- Second payment on account — 31 July 2027

- Balancing payment — 31 January 2028

Will There Be a Penalty System Under MTD?

At the moment it has been announced that MTD penalties for late submission of quarterly returns will not be applied for the initial year of MTD to 5 April 2027.

However, that should be balanced against the fact no mitigation has been announced for the penalty for failure to maintain digital records of up to £3,000.

We will be providing further details of the penalty regime under MTD separately.

How Can We Help You With MTD?

We will guide you through each stage to ensure a smooth transition to MTD.

In particular, we can assist you with MTD registration, reminder services for your records, preparation of digital records and submission of the required quarterly returns and annual returns as required.

You will not need to pay a monthly subscription for approved software because we provide this free of charge.

If you use software of your own choosing to prepare your records we can accommodate that with any provider, but please be aware that we would need to review the records prior to submission to identify any errors or omissions and any other adjustments.

You should also note that many companies are offering substantial introductory discounts for software over the transition period to MTD. These are generally restricted for a few months before the full price subscription becomes payable at significantly higher prices. Please aware of this.

We provide free HMRC approved software for clients using our quarterly MTD return service and can manage your digital records and the processing of your returns on your behalf.

Ultimately, your digital records will require analytical and other additional work before final accounts and tax calculations can be prepared.

Please contact Robert on his mobile number or our office number 0161 485 3027 if you have any questions or would like further clarification of any points arising.

We will be arranging registration for MTD for all of our existing clients.